The first official week of Summer has resulted in the largest week on week growth in capacity during the Covid-19 event with some 8.2 million seats added back around the globe and a week on week percentage increase of 21%. We may also be heading for a week with a very high rate of cancellations as airlines wait for demand to respond but let’s worry about that next week!

Capacity now stands at 41% of that available in the same week last year; some seven percentage points up on last week; quite a remarkable rate of growth as airlines, travellers and stakeholders around the world scramble to save the summer.

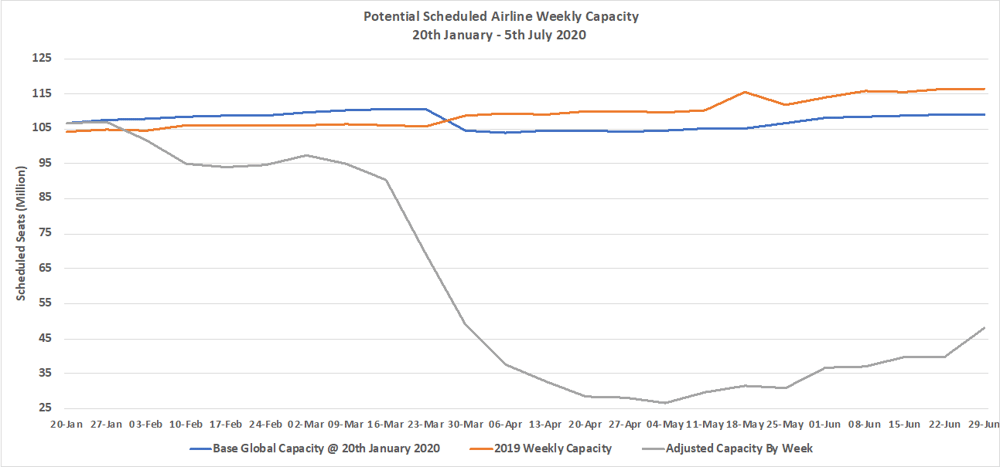

Chart 1 – Scheduled Airline Capacity by Week Compared to Schedules Filed on 20th January 2020 & Previous Year

Source: OAG

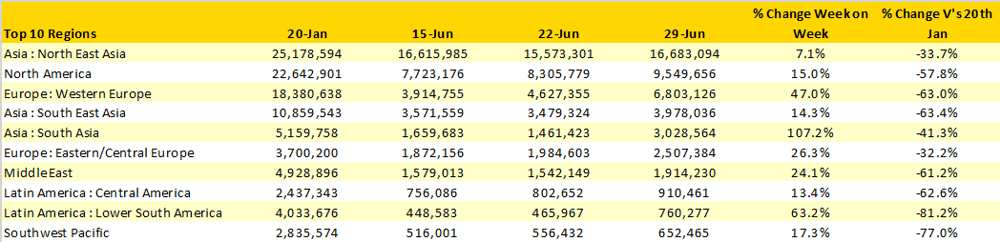

There are some quite remarkable rates of growth across the regions this week, in South Asia capacity has doubled week on week with an explosion of capacity in India where an additional 1.4 million seats will be added this week. In Europe capacity increased by nearly 50% as many major carriers upped capacity with Ryanair leading the way adding back over 450,00 seats, making them the largest airline operating in Western Europe this week.

Many regional markets now have capacity back to at least 25% of their January levels, the only exception being Lower South America where some countries continue to remain in lockdown whilst others such as Brazil are beginning to see rapid increases in domestic capacity as the country reopens. Interestingly this week over half of the new capacity has been added by legacy airlines who are slowly beginning to build back their networks.

Table 1 – Scheduled Airline Capacity by Region

Source: OAG

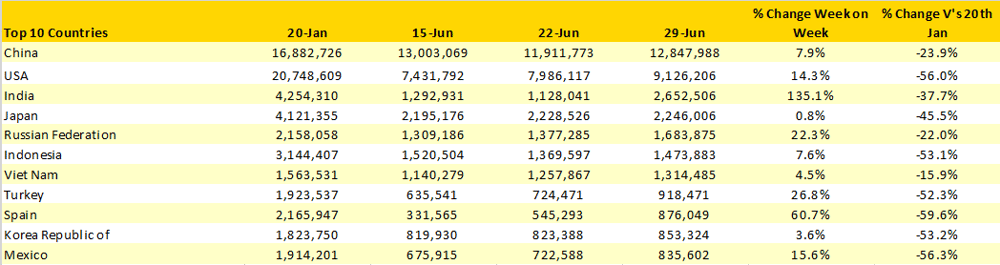

New entrants into the top ten country markets this week include Spain where a 61% increase in capacity week on week will not only be putting pressure on the airports but on the beaches as well. International capacity to Spain has increased by some 190,000 seats in a week with Ryanair adding back some 94,000 seats and easyJet returning to the market with scheduled services from many of their European bases.

China’s domestic capacity appears to have bounced back from last week’s lockdown in Beijing; total capacity increased by nearly a million seats with both Beijing airports reporting capacity growth this week. Chinese domestic capacity this week is at 86% of pre Covid-19 levels while international capacity remains at less than 10% of normal levels.

India’s rise to the 3rd largest country market reflects an additional 1.5 million seats coming back into the market this week with Indigo Airlines adding some 900,000 which is a 189% increase on last week’s capacity. However, that growth rate is beaten by GoAir who are reporting a four-fold increase in capacity this week. As we have tracked the recovery in the Indian market in recent weeks, we have noticed that cancellation rates have been quite low so it will be interesting to see if this capacity can be absorbed without a spike in cancellations.

Table 2- Scheduled Capacity, Top 10 Country Markets

Source: OAG

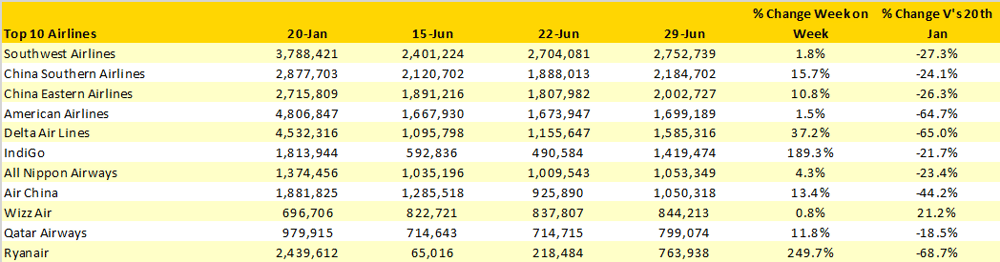

Delta Air Lines having added back over 400,000 seats this week have remained in fifth place amongst the top ten airlines which highlights how much fluctuation in the market exists; you have to grow capacity by some 37% just to remain in the same position this week! With Southwest Airlines remain the largest scheduled airline in the world this week with some 2.7 million seats on sale and three US and Chinese airlines in the top ten listing the importance of large domestic markets is clear for all to see.

This week some 624 airlines have schedules filed capacity; that compares with 709 airlines that operated in the week of the 20th January. Major carriers such as COPA Airlines, Jet2 and Tui Airways (UK) remain grounded although all have announced intended starting dates for services in July as conditions hopefully improve.

Table 3- Scheduled Capacity, Top 10 Airlines

Source: OAG

The arrival of July and the summer season has a feeling of optimism at last for the aviation industry, capacity has bounced back strongly this week; talk of travel corridors from the United Kingdom over the weekend resulted in a surge of booking activity and many markets around the world are reporting increasing load factors. An industry running at around 41% of its normal production levels is still a long way from where it should be, and we may have reached a capacity plateau for the next few weeks, but it feels a slightly better place than we were in two months ago!

This week will undoubtedly be a real test for both bookings and operational integrity, let’s keep our fingers crossed on both counts for a good week and some confidence returning.