Fed up with looking back at 2020 data we’ve sneaked a peek forward at how some of the major European low-cost carriers are viewing their Summer programmes; when it's dark and dreary outside thinking of the Summer sounds a great idea. Now, comparison with Summer 2020 is worthless and Summer 2021 still has a lot of shaping up but by comparing the coming Summer with the same period in 2019 we can get a sense of how they are feeling.

We’ve applied the principle of the “Big Three” and focussed purely on easyJet, Ryanair and Wizz Air; collectively they account for nearly half (46%) of all planned LCC services this summer so provide a representative feel for where these carriers see future demand. Total capacity between the three airlines for the Summer is currently set at around 138.4 million seats compared to 188.9 million in Summer 2019 so around three-quarters of what had been operated.

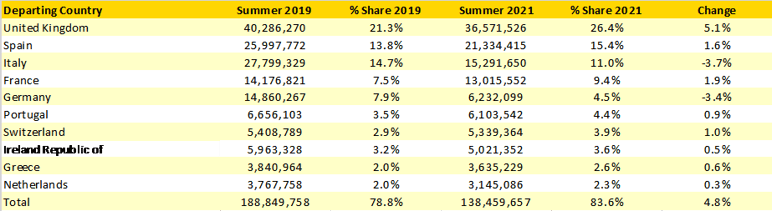

Banking on Brexit – The United Kingdom may finally have exited the European Union, but all three carriers are planning to increase the proportion of capacity that they operate from the UK this Summer as the table below highlights.

With some 36.5 million seats scheduled from the UK this summer the three airlines are looking to operate around 91% of their Summer 2019 capacity suggesting that they have more confidence in the market than most of the population have at this moment in time! With over one in four seats that these three airlines operate departing from the United Kingdom it also probably reflects a belief amongst the carriers that with vaccines arriving Island economies such as the UK will see significant and rapid demand stimulation; let’s hope so.

Italy and Germany are the major losers in capacity from these three airlines in Summer 2021. In the case of Italy, whilst the threat of a new lean Alitalia must have every other airline globally quaking in their boots the overcapacity of recent years is probably a more realistic driver of the capacity changes. In Germany a similar picture of over capacity will have been a factor but with 60% fewer LCC seats than in Summer 2019 it may be wise to grab a cheap fare whilst you can!

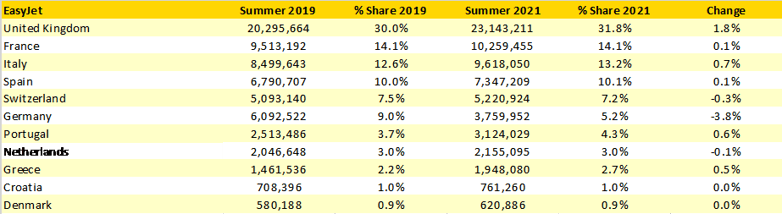

EasyJet Remains UK Focussed – despite closing three bases since Summer 2019, easyJet will continue to maintain a large UK presence with nearly one-third of their capacity departing from the United Kingdom. It seems a bold move to actually currently be offering more capacity from the UK this Summer, especially today, than in 2019 but strategically London Gatwick will be seen as increasingly attractive to the airline with some 46,000 services planned this summer, a 17% increase on 2019.

Germany is clearly not a market that easyJet expect to be easy this coming summer with a near 40% cut in planned capacity and with only 5% of their total summer capacity allocated to the market perhaps. Portugal and Greece are growth markets for the airline this coming summer with an additional half a million seats to both markets, Greece perhaps benefiting from having been open for most of last summer for holiday traffic.

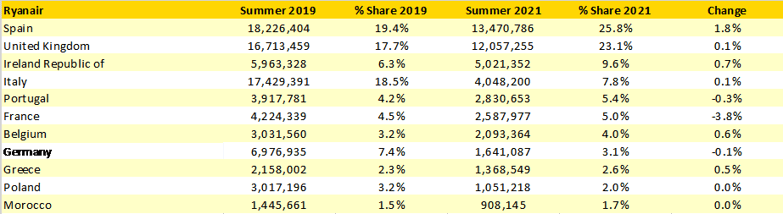

Ryanair’s Cautious Approach – Hard as it is to believe, Ryanair are currently scheduling around 52.2 million seats this summer which is some 42 million fewer than in summer 2019. Who would ever have thought of Ryanair as being cautious?

What can we make of that? Well, more capacity will be added in response to market demand and more airports can expect to have a discussion around fees and charges with the airline in the coming months! Also, you can only squeeze yield once capacity is being filled so this represents a careful and cautious approach from the airline.

It also reflects that when markets look tough it’s wise to retrench to the core programmes and there is nothing more solid than the UK – Spain market in any summer season; Ryanair know that and are banking on it! Nearly half of all Ryanair’s current planned capacity is between the two country markets and this is also one of the largest markets that responds to cheap fares, and no one loves a cheap fare more than Ryanair; accompanied of course by a very expensive baggage fee!

Perhaps the biggest change for Ryanair is their planned Italian capacity which currently shows a huge reduction compared to Summer 2019. Some 4 million seats in the system this week compared to over 17 million two years earlier suggest either a major change of strategic thinking, a falling out of love with pasta or a fear of lower cost competition from other carriers building.

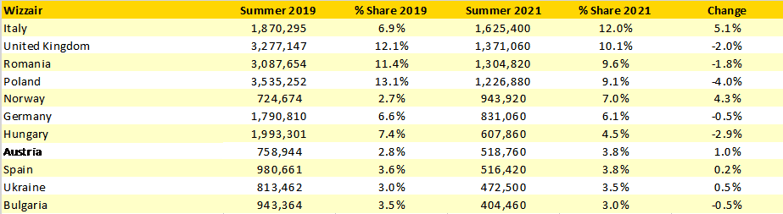

Wizz Air, To Boldly Go Where Others Went – although Wizz Air have only declared half of their hand by loading 13.5 million seats compared to the 27 million operated in Summer 2019 we can see what they are planning. Although in absolute terms Wizz Air have a slightly smaller number of seats in the Italian market it is currently their number one market for the summer: significantly ahead of its importance two years ago.

Wizz Air are also building their presence in Norway with a rapid build-up of capacity over the last half of 2020 where they have been seeking to take advantage of the demise of Norwegian and the large domestic market. Norway is currently the only country market where Wizz Air are showing capacity growth compared to two years earlier, but this is perhaps as much an early message of intent as anything else. Hopefully the experiences of others that have invested heavily in Spain and Norway will not be replicated again, and again!

Ultimately, we know that LCC’s are extremely flexible in their operation and can shift capacity around their networks at short notice as market conditions change. Early indications are that Spain, Greece and Portugal are likely to be the strongest markets for Summer 2021 and that Italy and German are the two markets where capacity is being taken out at the moment. All of which could of course change with a lockdown or quarantine announcement and one of those is always looming!