While legacy airline competitors are keeping an eye on how Norwegian Airlines fares with its long-haul low-cost flights on the Atlantic, long-haul low-cost options have been a regular feature of Australian international air services for some years. Are there lessons to be learned, and can we use the experience with Australia to predict the likely low-cost market share in long-haul markets?

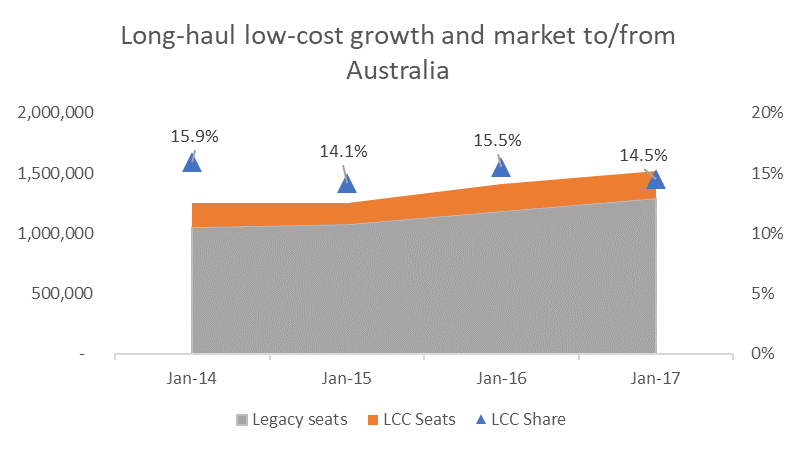

In September 2017, there were 1.5 million international airline seats available to and from Australia on routes over 4,000km. Of these, 14.5% were with low-cost airlines. While the long-haul market from Australia has grown by 21% between September 2014 and September 2017, the low-cost share has remained fairly static – 15.9% in September 2014, 14.1% in September 2015 and 15.5% a year ago. This is much lower than the typical low-cost share in short-haul and regional markets.

Through this period, two low-cost carriers have dominated the market, Australia-based Jetstar Airways with 47% of long-haul low-cost capacity, and Kuala Lumpur-based AirAsia X with 39%. Scoot operates a further 11% of capacity and Cebu Pacific the final 4%. While Jetstar has gradually added to its capacity, the other carriers have seen capacity grow and shrink in different years.

How does this compare to the evolution of low-cost airline capacity share more generally?

Low-cost airline capacity has been growing for decades, not just in absolute terms but also as a share of the total market. Back in 2000, low-cost carriers operated just 6% of airline seats. This had doubled to 12% by 2005 and was 20% by 2010. Today low-cost carriers make up 29% of scheduled airline capacity globally and the share appears to still be rising.

On transatlantic routes, where long-haul low-cost airlines are a more recent phenomena, low-cost capacity only makes up 5% of capacity.

Is the lesson from the established long-haul low-cost Australian market that expectations should be set at a maximum share of around 15% of the market for low-cost capacity? Maybe. Maybe not. Norwegian’s competitors on the North Atlantic will be watching and waiting.

Receive a weekly digest packed full of the latest insights

Trusted by 5,000+ aviation professionals

By submitting the form you agree to OAG using the information you provide to contact you about our relevant content, products, and services. You may unsubscribe from these communications at any time. For more information, check out our Privacy Notice.